After losing its grip in 2020, managed money is back in the driver’s seat pushing the price of gold and silver around. This analysis is written to explain the short-term price movements, which can be confounding given the strong fundamental backdrop. After very low volatility and a disappointing year in precious metals, it’s likely activity will pick up in 2022. Tracking the positioning of managed money will provide insights into the short-term price moves.

This article was originally published by SchiffGold.

Please note: the COTs report was published 1/3/2022 for the period ending 12/28/2021. “Managed Money” and “Hedge Funds” are used interchangeably.

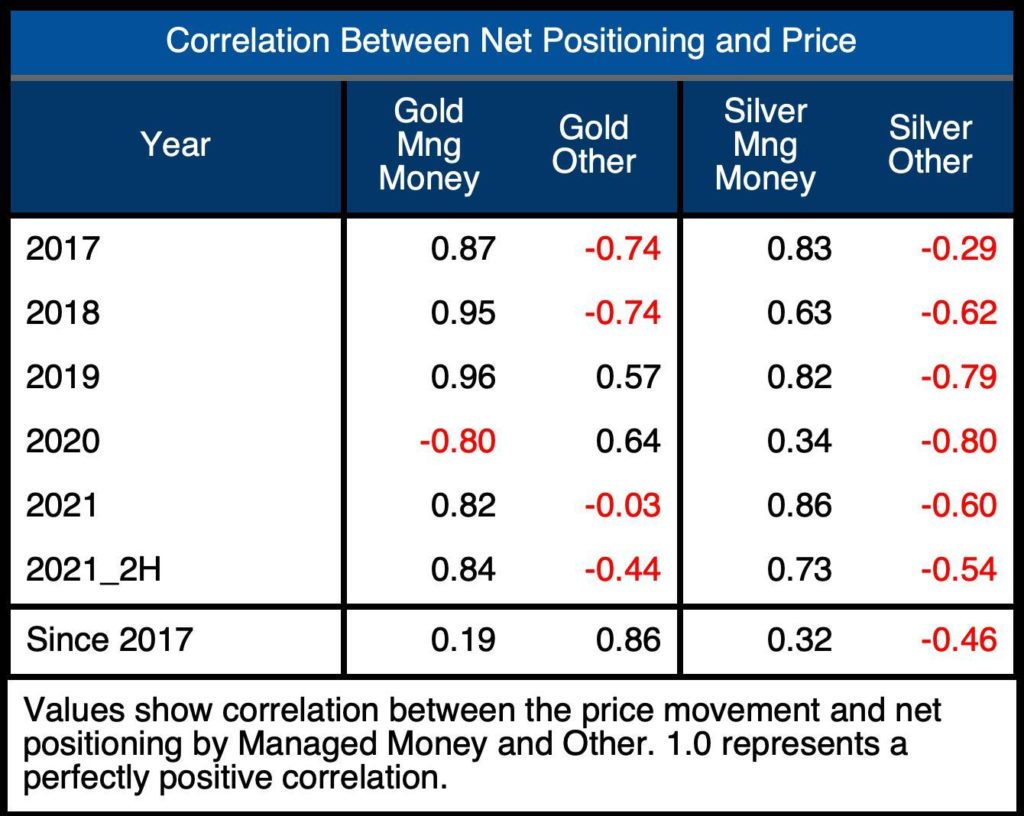

The Commitment of Traders analysis last month showed how much influence Managed Money has over the short-term price movement of gold and silver. The table below summarizes this influence by comparing the Managed Money Net Positioning with “Other”, the next largest category. Swap is not considered because it typically sits opposite the other two.

Figure: 1 Correlation Table

As shown in the table above, the influence of Managed Money is profound in the short term but much weaker over longer periods. Looking over the entire period since 2017 shows a much weaker correlation as the bull market marches on quietly under the volatile positioning of Managed Money.

That being said, the short-term is still driven by Managed Money net positioning.

In the most recent 6-month period, the correlation has become stronger in gold and weaker in silver (2021_2H is from July onward only). However, in both gold and silver, the correlation was quite weak in December as the analysis below shows.

Gold

Current Trends

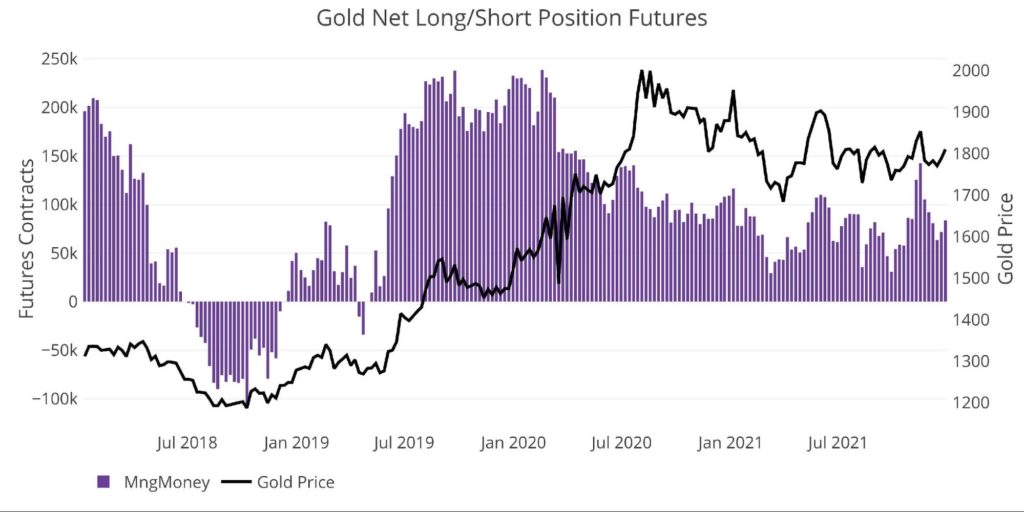

Over the last month, Managed Money net longs fell by 9% from 92k to 83k. Despite this net fall, the price of gold was up nearly $40 (as of last Tuesday). Unfortunately, Jan 3 saw the gains from the second half of the week wiped out.

On a year-end summary basis, the correlation is stronger. Managed Money net longs fell 23% over the course of 2021 from 108k on 12/29/2020 to 83k as of 12/28/2021 alongside golds fall of $70. Net longs are up 66% from three years ago on 12/31/2018 when net longs were 50k. Gold is up over $500 since then! Again, the monthly movement is strongly correlated, but over time, this correlation weakens as the bull market continues marching upwards.

Figure: 2 Net Notional Position

As shown above, “Other’ really built-up long positions in 2018 as the price fell. Managed money was liquidating the entire time, driving the price lower. As figure 1 shows, the correlation between the two was -.74 vs .95 in 2018. Essentially the entire price direction was driven by Managed Money. The chart below shows the strength of this relationship.

Figure: 3 Managed Money Net Notional Position

The chart above also highlights why 2021 has been so choppy. In past years, a steady direction was established in Maned Money net positioning. In the latest year, net positions were constantly bouncing up and down.

Weak Hands at Work

The chart below further highlights this trend, showing the week over week change for the past two years. The purple bars stick out with the erratic activity, constantly swinging from long to short.

Figure: 4 Silver 50/200 DMA

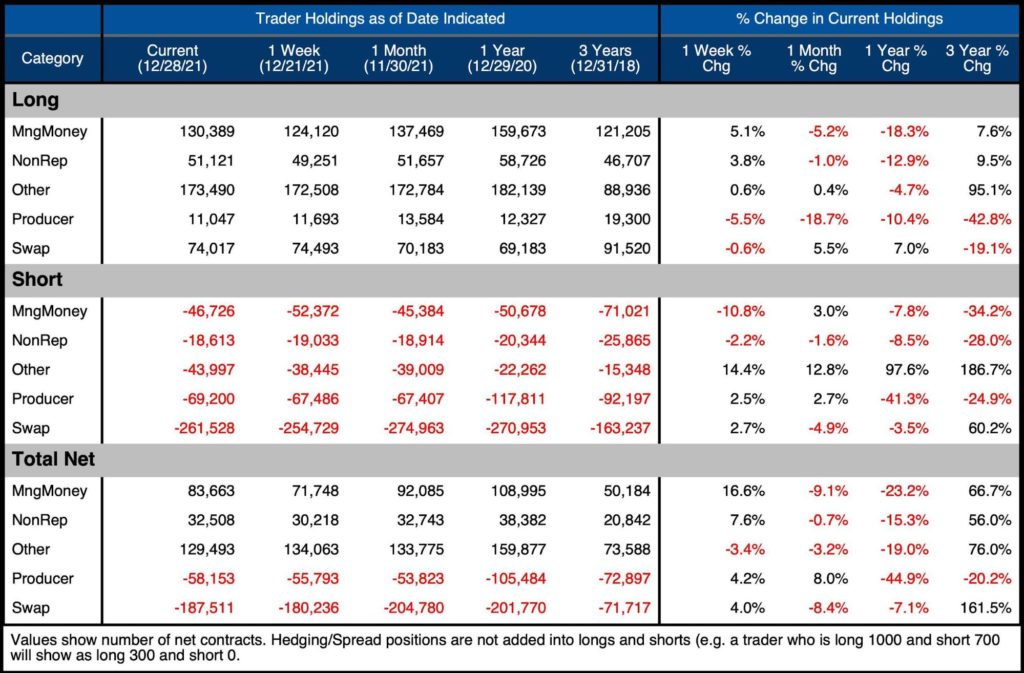

The table below has detailed positioning information. A few things to highlight:

- The Managed Money Net Long monthly decrease was driven primarily by longs liquidating

- Longs shed 7k contracts while shorts only added 1.4k

- In the last week of the year, there was a big move in longs and shorts, increasing net longs by 12k

- This partially explains the surge into the year-end close to $1830

- Most of these were most likely unwound on the first trading day – this will show on Friday’s report

- “Other”, which still represents the biggest Net Longs, saw 4k net long reduction

- This was driven entirely by increased short positions

Figure: 5 Gold Summary Table

Historical Perspective

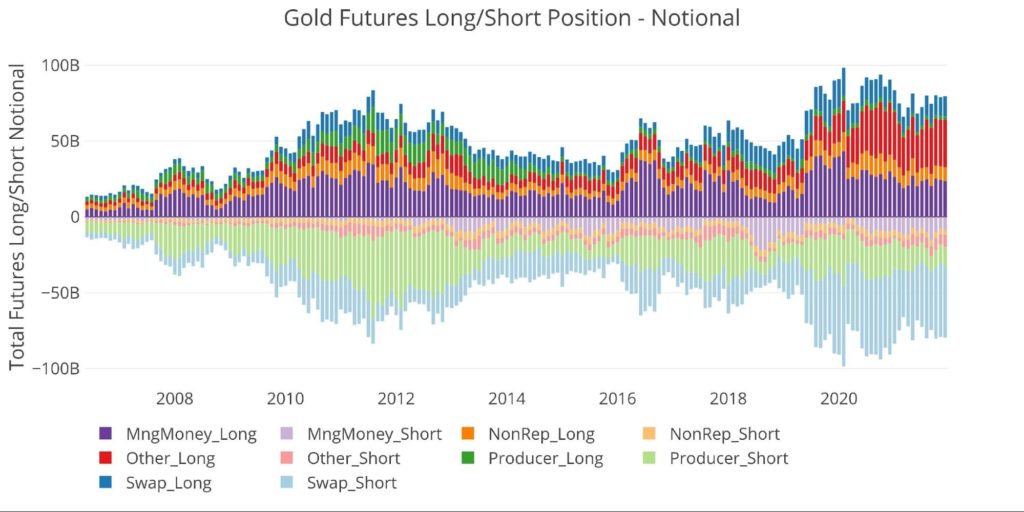

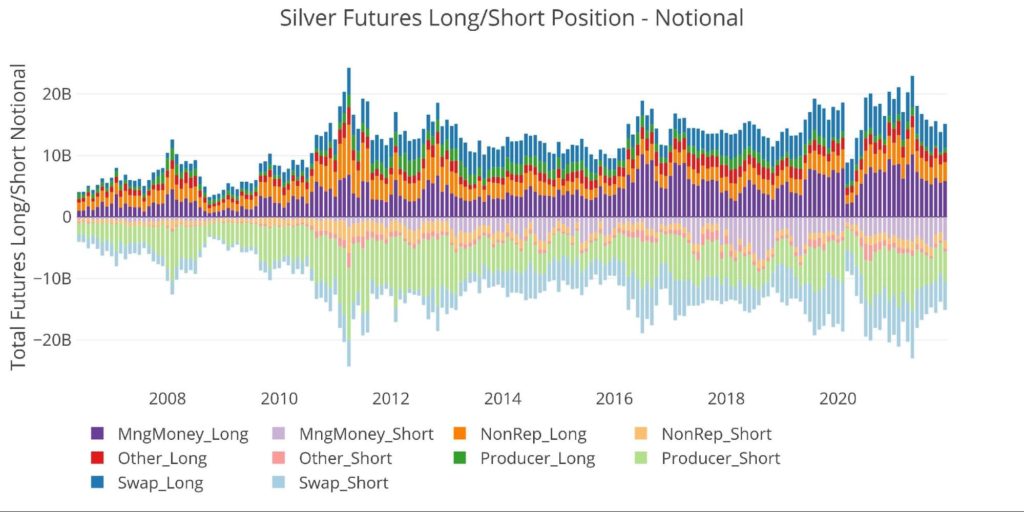

Looking over the full history of the COTs data by month produces the chart below (please note values are in dollar/notional amounts, not contracts). The chart shows the last run-up in price in 2011, followed by the slow fall into 2015 until the new bull market started in 2016.

This chart also shows how big the “Other” category has become on the long side. In 2011, Other Long had $8.6B in gross long vs $31.4B in the most recent period.

Figure: 6 Gross Open Interest

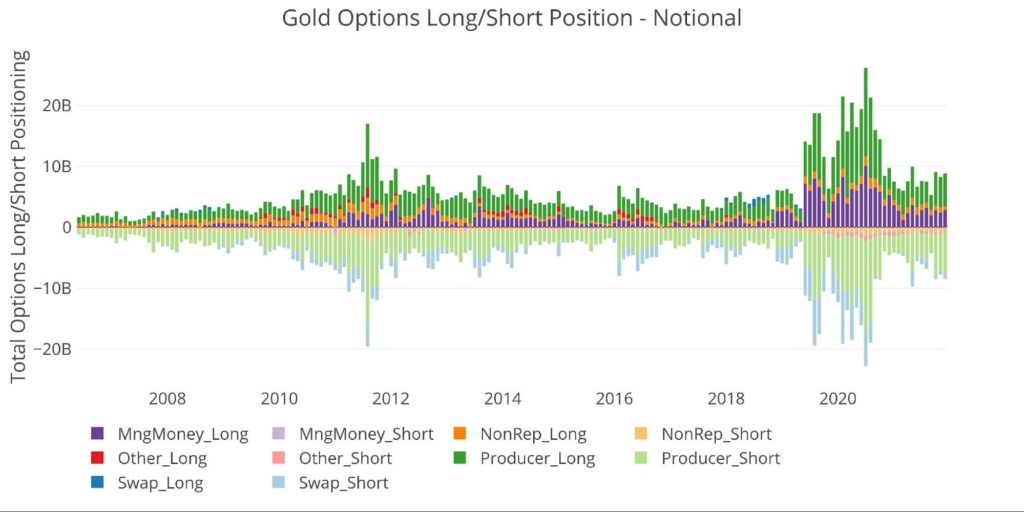

The CFTC also provides Options data. This has mainly been dominated by Producers, but recently Managed Money has played a larger role within the market. The current period shows a counter-trend with Managed Money Longs increasing from $2.4B to $2.8B during December. Perhaps this helps explain the point mentioned above how the price still moved higher despite lower future positioning.

Figure: 7 Options Positions

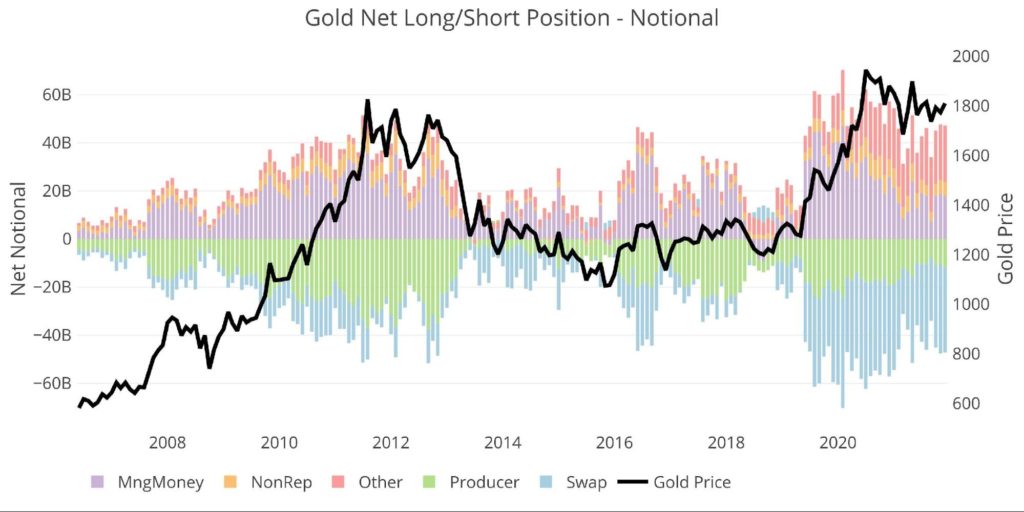

The final chart below looks at net notional positioning against price on a longer time frame. As mentioned, while the correlation of managed money is strong, it is not perfect. The long-term bull market continues despite the volatile gyrations of managed money positioning.

Figure: 8 Net Notional Position

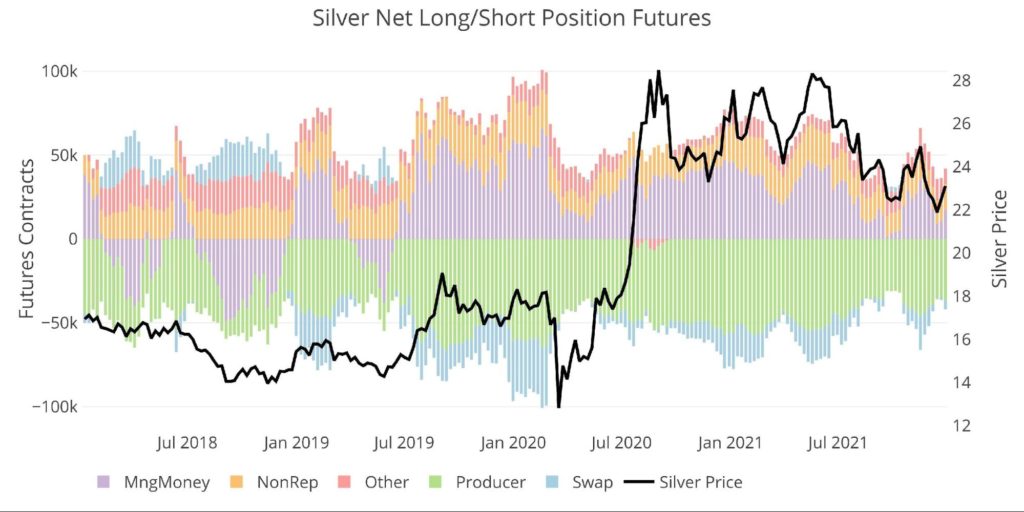

Silver

Current Trends

Silver was also not entirely driven by Managed Money. Net positioning fell at the start of December and only increased meaningfully in the final week.

Figure: 9 Net Notional Position

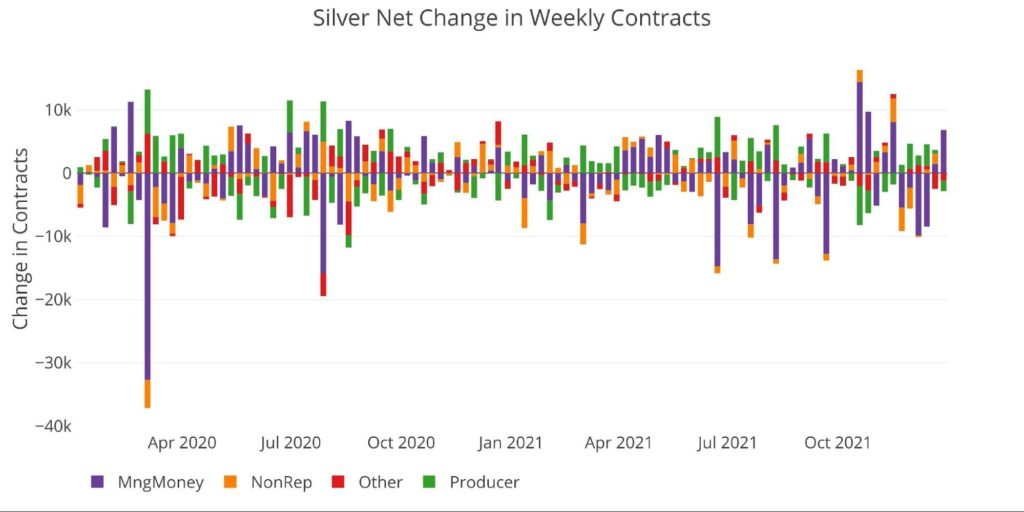

This can be seen more clearly in the weekly chart. Managed money dropped net longs for four straight weeks in late November into the Fed meeting in mid-December.

Figure: 10 Net Change in Positioning

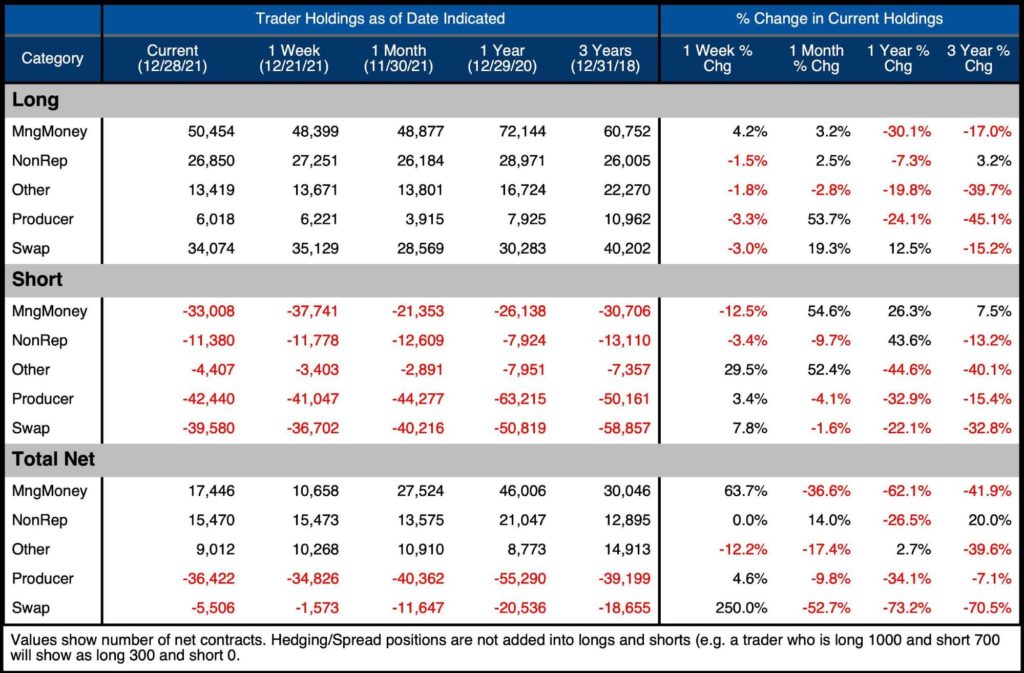

The table below shows a series of snapshots in time. This data does NOT include options or hedging positions. Important data points to note:

- Managed Money change was driven primarily by short

- Shorts increased positions by 54.6% over the month

- Longs only increased by 3.2% resulting in a net fall of 36.6%

- The final week saw longs increase and shorts decrease, softening the blow

- Non-Reportables was the lone entity increasing net longs

- Producers also decreased their net short by adding to gross longs

Figure: 11 Silver Summary Table

Historical Perspective

Looking over the full history of the COTs data by month produces the chart below. The chart shows the last run-up in price in 2011, followed by the slow fall into 2015. The price collapse in silver in 2020 is clearly visible in this chart. As can be seen, gross longs are still well above the 2020 lows.

Figure: 12 Gross Open Interest

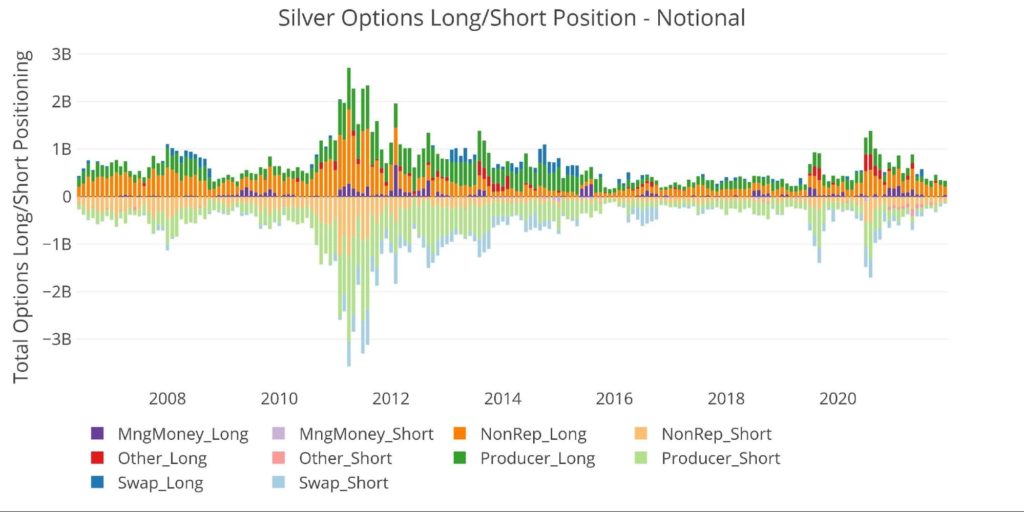

The CFTC also provides Options data. This has mainly been dominated by Non-Reportables, exceeding even Producers. Options have fallen off significantly from the spike last July and is still well below the peak in 2011.

Figure: 13 Options Positions

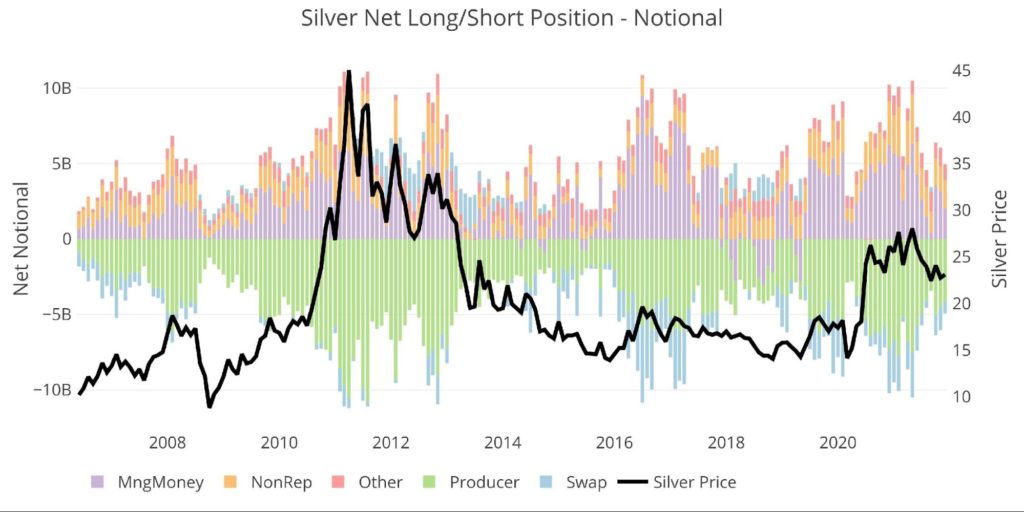

Finally, looking at historical Net positioning shows the correlation of positioning with price. Similar to gold, the peaks and valleys in price are mirrored in the open interest.

Figure: 14 Net Notional Position

Conclusion

Managed Money tends to push the price around, but the long-term bull markets in gold and silver persist under this activity.

Astute investors should keep the long-term picture in mind. The short-term gyrations can be immensely frustrating, but gold and silver are not Bitcoin. They are not vehicles to get rich quick because that would disqualify them as safe-havens. Remember, what goes up quickly, can come down quickly. Stay the course, trust the fundamentals, use the CFTC analysis to explain the short-term price movements, and understand the protection provided by physical precious metals.

Data Source: https://www.cftc.gov/MarketReports/CommitmentsofTraders/index.htm