Cobras, Windows, and Executive Compensation Part II

In Part One of this series (Tales of Cobras, Windows, and Economic Promise), we discuss the “cobra effect.” It is a term that derives from a venomous cobra outbreak in India. We chose this tale to exemplify how solutions to problems, on occasion, have the opposite of the intended effect.

In this article, we present a two-headed cobra effect. First, government legislation designed to limit executive compensation and second, the influence of economists and academia to base executive compensation on “performance.”

Bush vs. Clinton

In the early 1990s, like today, there was a disproportionate gap between corporate executive compensation and employees. There was also discontent from academia that the level of executive compensation was not justifiable based on performance. Many leaders thought that closing the compensation gap would benefit employees and the economy.

At the time in 1992, there was a presidential election between George Bush, the sitting President, and the two-term governor from Arkansas, Bill Clinton. Part of Clinton’s campaign pledge was to tame what he deemed “excessive executive pay.”

Specifically, Clinton intended to reverse a recent veto by President George Bush, limiting corporate tax deductions for executive compensation.

Elected in November of 1992, Clinton soon after signed into law section 162(m) of the IRS code. The code limits corporate deductibility of executive pay to $1 million for “named executives” at publically traded companies.

Financially penalizing companies with high wage-earning executives may seem like a smart way to limit compensation. Then again, putting a bounty on cobra heads also seems like a reasonable way to get rid of cobras.

30 years later

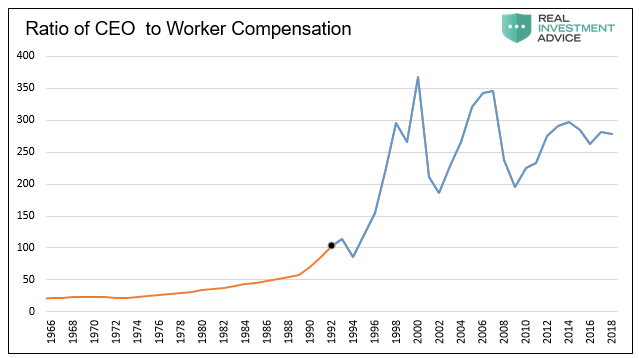

Now, 30 years later, we can clinically evaluate the effectiveness of that legislation. The graph below illustrates one measure comparing executive pay to worker compensation.

Data Courtesy: The Economic Policy Institute

Executives tend to have excellent legal counsel and they employ the best accountants money can buy. That being the case, they quickly found ways to avoid the penalties imposed by Clinton’s legislation. Essentially they would limit their traditional take-home pay and increase other forms of compensation. Most notably, stock and stock option awards.

The graph below shows a distinct change in the makeup of compensation packages starting in 1992. While the graph is only through 2008, the trends continue to this day.

Executives not only helped their company’s tax planning but increased their pay immensely. Changes in pay structure were pleasing to economists and academia who were of the belief that economic progress excels with performance-based compensation.

However, the definition of performance has different meanings to different people.

Incentives

Stock-based compensation as a percentage of total executive compensation has proliferated since 1992. Laws written and passed based on “sound academic analysis” radically modified incentives.

A person paid in stock will be motivated to get the stock to trade for as high a price as possible. Logically, the next issue to analyze is the correlation between stock performance, long-term corporate profitability, and employee welfare.

According to research from the Harvard Law School Forum on Corporate Governance, since 1990, CEO median pay at large U.S. corporations has grown 514% adjusted for inflation. Over the same period and on an after-inflation basis, median household income has increased by 21%, GDP slightly less than 100%, and S&P 500 earnings by 129%.

Such massive outperformance of executive compensation over corporate and economic performance is telling. As CEO pay becomes more closely aligned with the stock price, CEOs and executive leadership, in general, target corporate decisions which drive share prices higher. These include cutting expenses, leverage up the company, neglect investments into the future, and of course, manipulate the stock price via share buybacks.

With a focus on share prices, not only do corporate profits suffer but so do economic and productivity growth. Executives grew more prosperous at the expense of the economy and a large segment of the population.

Sowing the Seeds

It is easy to blame political leadership and their legislation, but they had a lot of support. As noted, at the time, academia lobbied for performance-based executive compensation in the name of enhancing “shareholder value.” They theorized that basing pay on performance would solve the compensation problem. This line of thought was not new. They were parroting what economists were saying over the prior 20 years. In Short Term Gain – Long Term Pain, we wrote the following:

“In the early 1970’s, economists began to argue that the motives of agents (executives) were different from those of the principals (shareholders), thus in their opinion, a principal-agent problem existed. To align the interests of executives and shareholders, economists promoted a theory that executives should be given financial incentives derived from corporate stock performance.”

With the “do-gooder” economists, think tanks, and large universities behind him, Clinton enacted legislation that laid the groundwork for economic failure. They put a bounty on cobras without considering that executives would begin breeding them for income.

Simple Fix

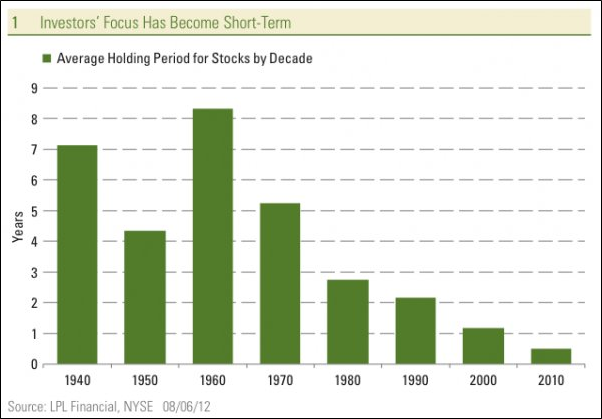

One would think that shareholders would be aghast at what has occurred. They are not, and for a good reason. The average holding period of stocks has shrunk from eight years in the 1960s to less than one year today. While the graph below is dated, we venture the current holding period indeed has not lengthened. Most investors are no longer “investing” as part owners in a company. They have become stock renters, flipping electronic pieces of paper with a click or two of a mouse.

Short-term shareholders do not care about long-term corporate performance. Buybacks are cheered and will always trump investments into a company’s future.

The fix is easy. Pay executives on metrics related to corporate profitability in the future. Force their attention to that which is best in the long run for shareholders, employees, and the communities they operate in. Not only will shareholders prosper, but workers and the economy will as well. It may be wishful thinking given the power structure. Still, corporate, economic, and monetary policies must be re-aligned away from short-termism and expediency to those which will deliver organic growth and long-term prosperity.

Summary

What started in 1992 as a seemingly noble idea to shrink the wealth gap and income disparity now quite clearly has only made the problem worse. Poorly thought-out legislation hurt productivity growth, economic trends, and the prosperity of almost every citizen.

The solutions for solving some of our economic woes are neither complex nor difficult. They will, however, require sacrifice to establish proper incentives. Much of that sacrifice falls on the top 1% who benefit the most from an artificially inflated stock market.

As we hope you will notice with this series of articles, the rationale and justification for addressing a problem are often well-founded. Still, the resulting incentives borne out of the “solution” can lead to viperous unintended consequences.