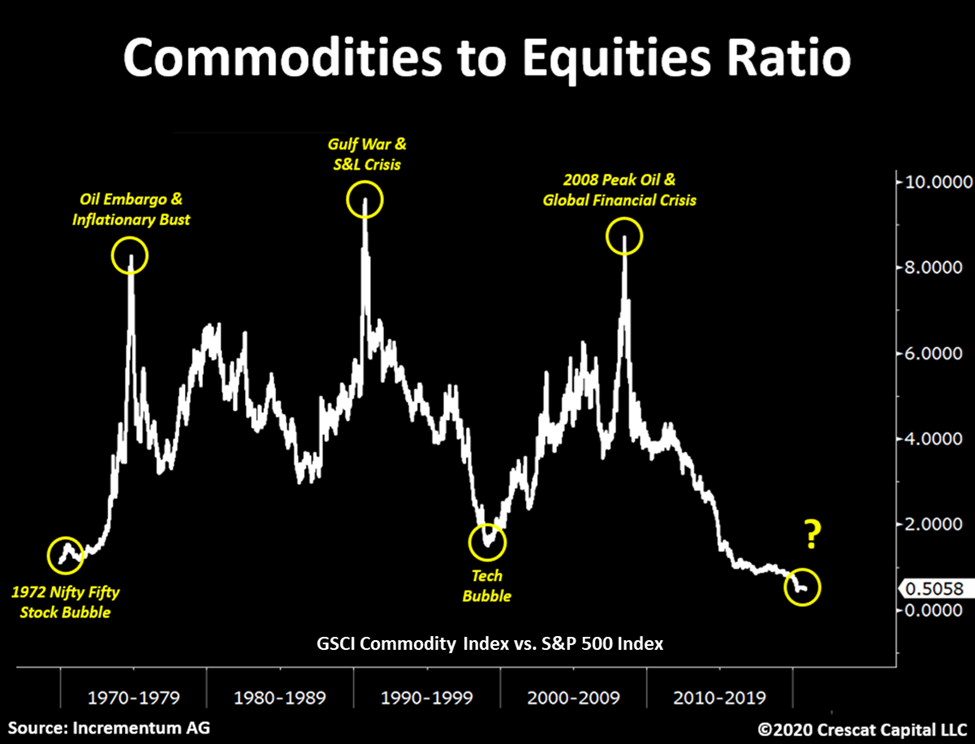

Markets are cyclical. Today, stocks trade at record high valuations while commodities are historically undervalued in relation. The setup is in place for a macro pivot in the relative performance of these two asset classes. Comparable conditions were present with the 1972 Nifty Fifty and 2000 Dotcom bubbles as we show in the chart below.

As capital seeks to redeploy towards the highest growth and lowest valuation opportunities, we expect analytically minded investors will soon be rotating, if not stampeding, out of expensive deflation-era growth equities and fixed income securities and into cheap hard assets, creating a reversal in the 30-year declining trend of money velocity.

Today’s Modern Monetary Theory world with its double barreled fiscal and monetary stimulus is crashing head on with an accumulation of years of declining investment in the basic industries such as materials, energy, and agriculture. In our analysis, the “end game” for the Fed’s twin asset bubbles in stocks and bonds is inflation. We can already see it developing on the commodity front.

The scarcity of jobs and abundance of debt were factors preventing the economy from reaching its full growth potential even before Covid-19. Such have been the concepts underlying the output gap, the theoretical paradox that is thought to have held inflation in check over the course of the last business cycle. But based on comparable historic periods, the macro setup for inflation is more likely to be kicked off by an input gap, i.e., shortages in the primary resources needed for both a strong reserve currency and economic growth at the same time as policy makers pull out their biggest bazookas yet to boost aggregate demand. We expect a new wave of rising commodity prices, set up by past underinvestment in basic resources, to soon ripple through the global supply chain creating a headwind for real living standards. Welcome to the Great Reset.

The global economy is at risk of commodity supply shock inflation, something we have not experienced since the 1970s. Both the Bloomberg Commodities Index and the US 30-year inflation expectations are now re-testing a 12-year resistance line. A significant breakout from here would be a big shift in the macro investing landscape. Yes, the aging demographics problem and significant technological advancements are deflationary tailwinds. But in our view, the key reason why consumer prices have not gone higher is due to a long-standing period of depressed commodity prices, a trend which we think is about to change.

The Constrained Supply for Gold

When it comes to scarce commodities, at Crescat, we have an affinity first and foremost for gold and silver, the monetary metals that are among the most supply constrained resources on the planet. Coincidentally, they are facing a new surge of investor demand.

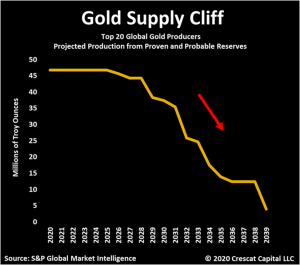

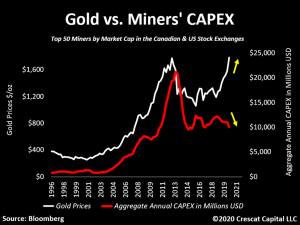

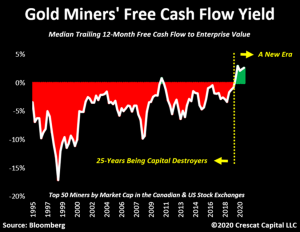

On the supply side, in the disinflationary environment since the precious metals mining industry’s prior peak in 2011, gold and silver miners have been criticized by investors as being capital destroyers. As a result, the industry’s spending discipline in the last decade has swung completely the other way. The majors have underinvested in replacing their reserves creating a supply cliff for the industry while also substantially boosting free cash flow.

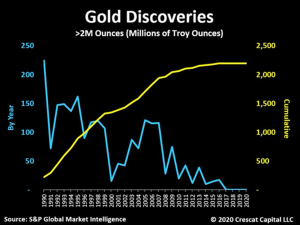

Contributing to the supply shortage, the number of major new gold discoveries by year, i.e., greater than 2 million Troy ounces, has been in a declining secular trend for 30 years including the cyclical boost between 2000 and 2007. At Crescat, we have been building an activist portfolio of gold and silver mining exploration companies that we believe will kick off a new cyclical surge in discoveries over the next several years from today’s depressed levels.

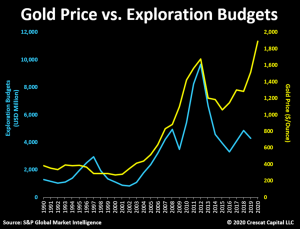

Gold mining exploration expense industrywide, down sharply since 2012, has been one of the issues adding to the supply problems today. Crescat is providing capital to the industry to help reverse this trend.

Since 2012, there has also been a declining trend of capital expenditures toward developing new mines. From a macro standpoint, gold prices are likely to be supported by this lack of past investment until these trends are dramatically reversed over the next several years. Credit availability for gold and silver mining companies completely dried up over the last decade. Companies were forced to buckle up and apply strict capital controls to financially survive during that period. Investors demanded significant reductions in debt and equity issuances while miners had to effectively tighten up operational costs, cut back investment, and prioritize the quality of their balance sheet assets.

It is important to consider that the last times this industry had been acting in a similarly conservative fashion, metal prices were at historically low-price levels. This time, however, we are seeing corporate discipline with gold prices remaining near all-time highs. As a result, the major producers today have surprisingly swung into being cash flow machines. They are enjoying more free cash flow than they had in the past 25 years, an incredibly bullish setup for the entire industry, especially the smaller exploration focused players that Crescat is overweight in today. The majors are in a great position to harvest cash for the next few years. But they are also facing a supply cliff because they have not replaced their reserves. Over the next several years, they will need to make acquisitions in the exploration segment to rebuild them.

The Demand Side for Gold

The Demand Side for Gold

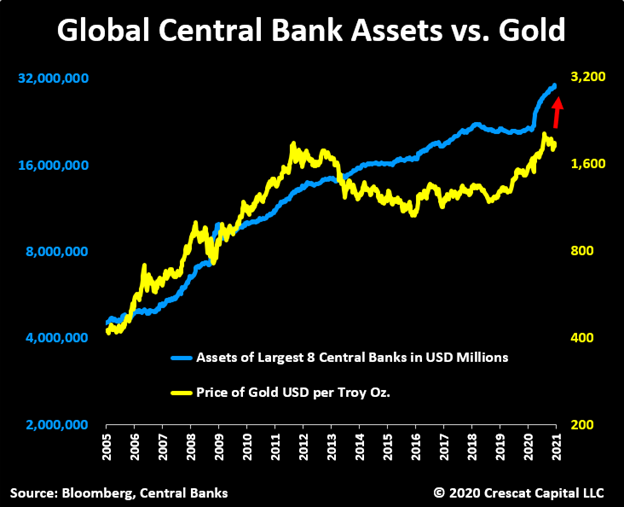

On the demand side, the first key macro driver for the price of gold is central bank debt monetization, which drives increasing inflation expectations and investor demand for inflation protection for accumulated savings. Today, money printing through central bank balance sheet expansion is widely accepted and embraced. It is the only viable policy as a way out of the otherwise deflationary global debt burden, at a historic high of 365% of worldwide GDP. With deficits at World War II levels in the US, we expect money printing to be the path of least resistance among policy makers towards easing debt burdens and reconciling many of today’s economic imbalances, though it will likely come at a cost to savers who are invested in overvalued traditional financial assets.

As we show in the chart below, gold underperformed the pace of global money printing from 2011 to 2018. But since the Repo Crisis in 2019 and the coronavirus led recession that followed, global QE has been accelerating to the upside once again. Gold is being pulled up with it. Our near-term target price for gold is north of $3,000 per Troy oz. based on our macro model shown below that plots the price of gold vs. the aggregation of the top eight central bank balance sheets. This target will almost certainly be rising in the near-term with $5.8 trillion just in US Treasuries alone maturing in 2021 and much of that needing to be rolled over and funded by the lender of last resort.

The Fed, the printer of the world reserve currency, has given itself, and by extension its central bank counterparts around the world, the green light to err on the side of inflation. The US central bank has declared that it can exceed its 2% inflation target temporarily abandoning one side of its dual mandate to favor the other side of it which is full employment. So, err on the side of inflation, the Fed almost certainly will.

Inflation is a toothpaste that sovereign Treasuries and their central banks throughout history have struggled putting back in the tube once they have let it out. In practice, inflation is driven in large part by the expectations and actions of consumers and investors which are hard to predict and occur with lags and unknown multiplier effects in relation to monetary policies. When consumer and investor psychology shifts toward recognizing and acting upon rising inflation, it becomes highly reflexive, i.e., circular and self-reinforcing.

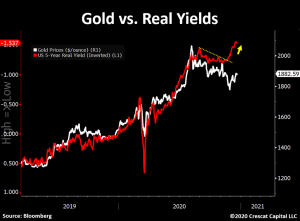

The second key macro driver for upward trending gold prices on the demand side today is declining real interest rates, which are a combined reflection of central bank interest rate suppression tactics and investors’ rising inflation expectations. The recent plunge lower in real yields (shown inverted in the chart below) has diverged from the price of gold signaling a strong impending move upward again in the metal.

The outlook for gold all ties back to the bigger macro imbalances we see in the US economy today. The Federal Reserve is crippled in its ability to prevent inflation and instead has become the funding mechanism through its massive purchases of US Treasuries that enables the US government to run a large fiscal deficit. The Fed essentially has no independence in the matter. It must fund the government’s fiscal stimulus programs as the lender of last resort. And as the repo crisis showed, the liquidity is also necessary in the short run to prevent the equity and corporate bond markets from collapsing, but this is very shortsighted because rising commodity prices and real-world inflation, that is the byproduct of the newly printed money, is the killer of record overvalued financial assets.

Three Comparable Macro Setups in History

We expect inflation expectations to continue to rise at a faster rate than nominal interest rates. This is ultimately a self-reinforcing catalyst to drive investors out of overvalued stocks and credit and into scarce commodities including precious metals and oil, which is exactly what happened in three similar macro setups to today:

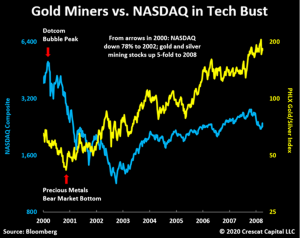

1. During the dotcom bust at the turn of the century, the NASDAQ Composite declined 78% over two and a half years, a period during which gold stocks diverged to the upside to begin a five-fold march upward over the next seven years, while energy and industrial commodities also caught fire.

2. In the 1974-74 bear market, the S&P 500 declined 50% in two years while gold mining stocks increased five-fold at the same time as oil prices skyrocketed during the 1973 Arab Oil Embargo and a decade of stagflation was born.

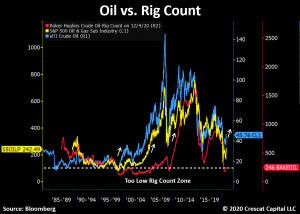

We showed the supply cliff setup for gold earlier, but it is important to note that there could also be a supply shortage in oil setting up for the next several years after the most drastic capex cuts in infrastructure and exploration we have seen in the history of this industry. In that vein, the rig count cyclicality has been an incredibly reliable contrarian forward looking indicator for oil prices. As shown in the chart, prior historical dips also preceded key market bottoms in WTI prices and the oil and gas industry.

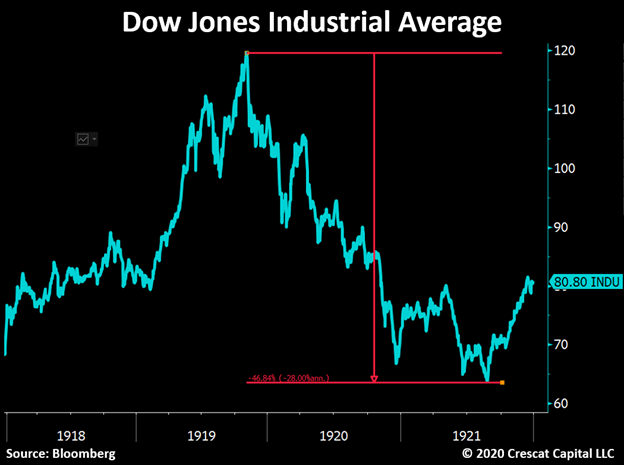

3. The third comparable period, also highly apt for today, was coming out of the Spanish flu pandemic of 1918 and 1919. At that time, the health crisis had severely limited the industrial capacity of the economy, leading to major supply shortages of raw materials and causing commodity inflation at the same time as the world began to heal. The rise in wholesale prices became a global phenomenon. Grocery stores began hoarding inventories to sell at higher prices, forcing governments to intervene and criminalize these actions to avoid an even larger hit to the consumer. The cost of living surged and prompted major labor union protests on the streets demanding higher wages and salaries only exacerbating the problem. Inflation spiked above 20% in 1920 and the Dow Jones Industrial Average began a decline of 47% from peak to trough from 1920 to 1921 while the world emerged from the pandemic. We will not go there in depth now, but this was the same time that a whole different kind of inflation was arising in Germany from newly printed money to pay off accumulated war debts.

The Opportunity for Activist Gold Exploration

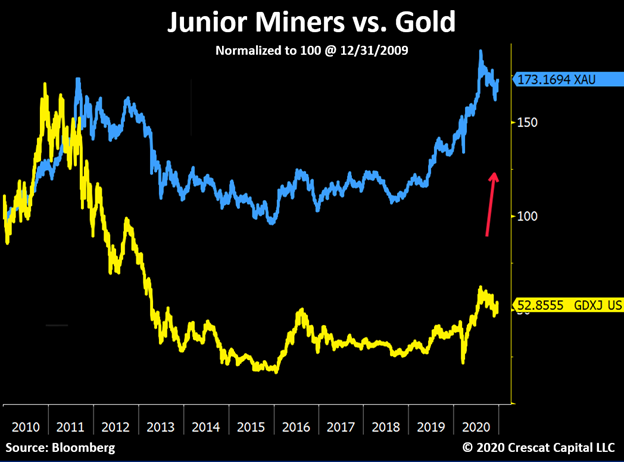

As we showed above, the underinvestment in most of the last decade in the gold mining industry will soon send the majors scrambling to invest their near term soaring free cash flow in the most prospective new gold and silver deposits being explored today. These properties are in the hands of the extremely undervalued and ultra-depressed small cap segment of the mining industry, the junior explorers, a group that has been through a brutal, capital starved bear market that effectively lasted ten years. The whole industry completed a double-bottom retest by successfully holding above its 2015 lows and rebounding sharply to lead all industries in stock price performance coming off the March 2020 correction. We think there is much more performance ahead for this industry as it is still in the early stages of a new secular bull market.

We are confident that within the precious metals mining industry, the most value for shareholders will be created from the small cap exploration segment over the next several years. We think Crescat’s Precious Metals Fund and SMA strategies have already started to demonstrate that potential in 2020.

By working with world-renowned exploration geologist, Quinton Hennigh as Crescat’s geologic and technical advisor, Crescat has already created an activist portfolio of over 50 companies where we are among the largest shareholders of a targeted 200 million ounces new high-grade gold equivalent discoveries. We plan to continue to grow these targeted ounces while getting the needed investment capital to our companies to prove out these economic deposits through drilling and discovery.

Crescat’s activist fund is a large and significant capital deployment opportunity. We are currently seeking a select group of right-minded institutional partners who can understand and appreciate the focus, scale, and timeliness of what we have set out to accomplish in this fund.

Our activist portfolio is positioned ahead of a likely major new wave of M&A by the large and mid-tier producers which is still to come as they necessarily must replace their reserves through acquisition. We also have a handful of holdings that we call keepers, the cream of the crop companies that control the unquestionably new world class, high grade gold and silver deposits that will catapult them into the next great mid and large cap gold producers in the industry over the course of the new secular bull market.

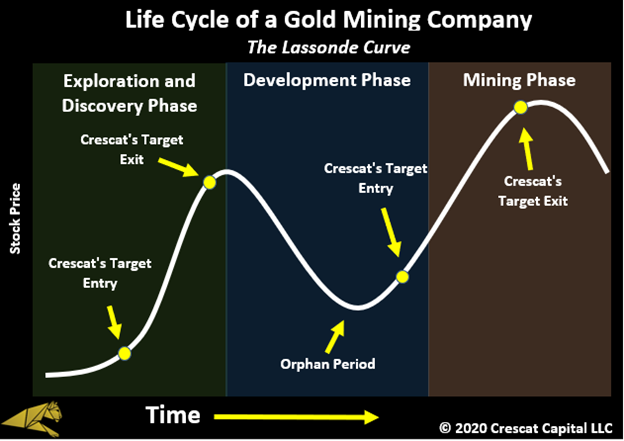

To be frank, buying gold or silver is not a contrarian investment position today. There are enough people in agreement with the idea that all government backed fiat currencies are doomed to some level of devaluation through inflation due to the level of fiscal and monetary imprudence and unsustainable debt imbalances in the financial system. Naturally, with a constructive view on precious metals, the next step for most investors is to start dipping their toes into well-known and established mining companies. Despite their past reputation of being capital destroyers, investors today are warming up to the idea of buying the “Newmonts and Barricks” of the world or even ETFs such as GDX and GDXJ. What we see as contrarian, however, is a much bigger opportunity to unlock value through a well targeted activist strategy in the exploration segment of the industry. No doubt, many are skeptical of the gold exploration business, given its poor performance during the last downturn in the industry at large, but the biggest gains today in the industry are likely to come from what are the smaller cap names. Between Crescat and its 21 years of money management experience and Quinton Hennigh with his 30+ years of gold mining exploration experience to serve as Crescat’s geologic and technical advisor, we believe we have the expertise and preparedness to navigate this incredible opportunity before us. We hope you will join us as we seek to exploit the mispriced opportunities on the exploration and discovery side of the Lassonde Curve that is still in the early stages of what is likely to be a new rip-roaring secular bull market for precious metals.

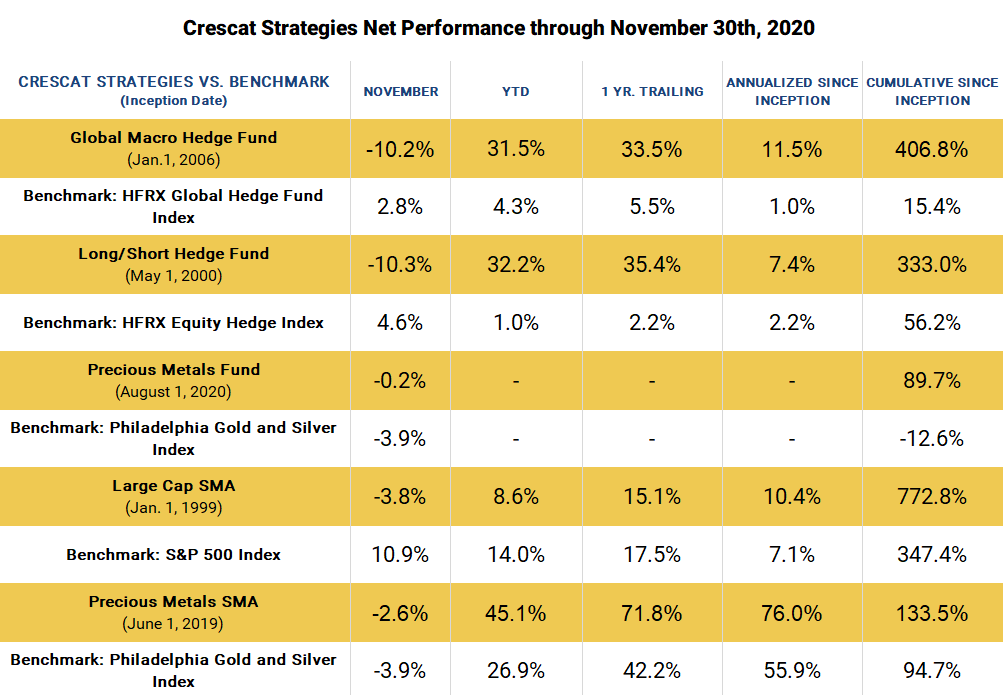

Performance

This article was published by Crescat.net.