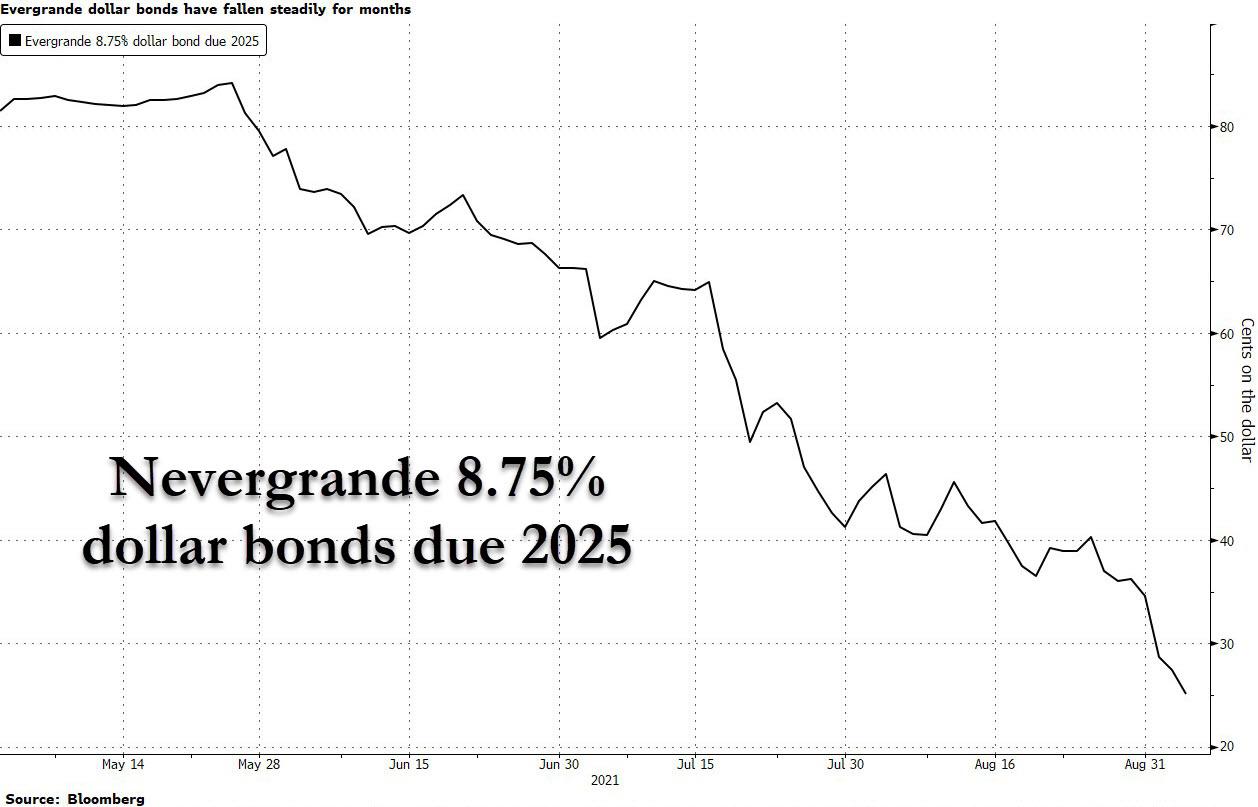

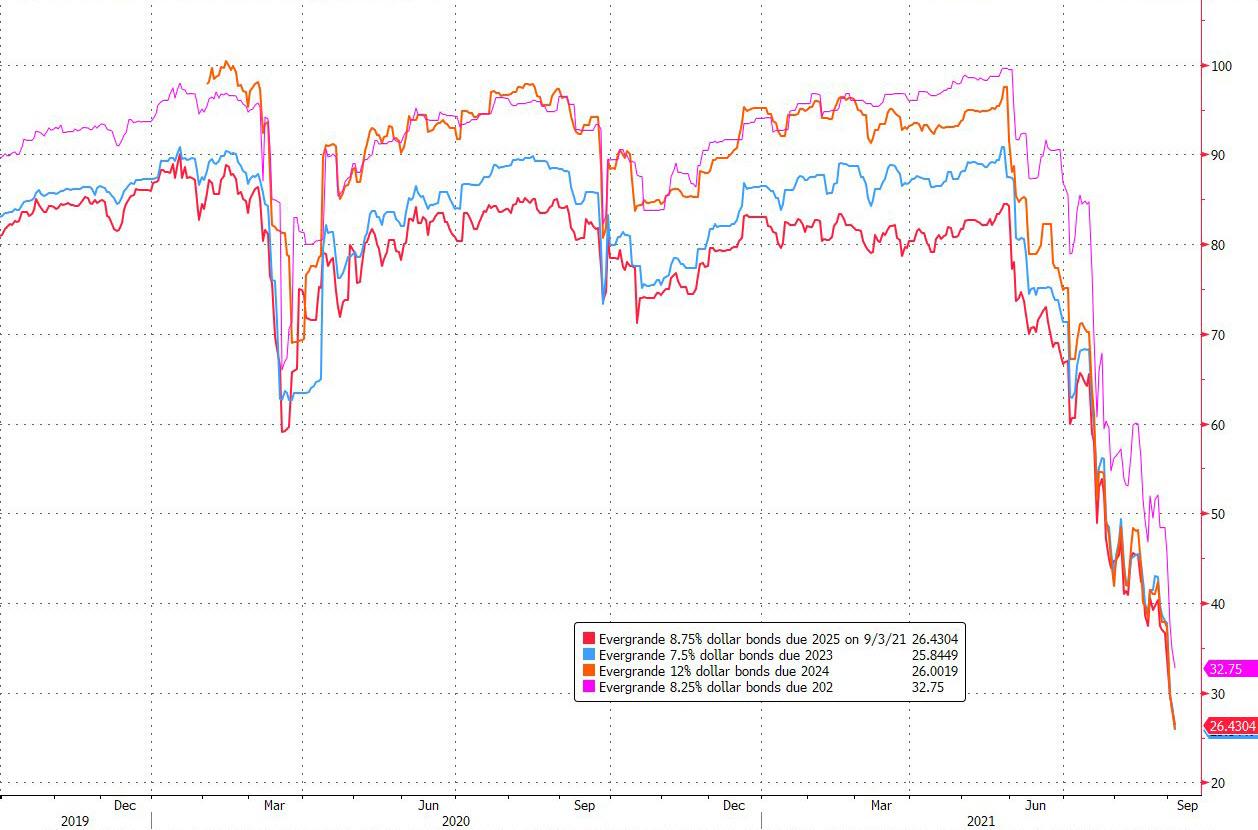

With algos busy chasing upward momentum in futures and global stocks, the biggest – if largely ignored story – remain the ongoing collapse of “China’s Lehman“, the $300+ billion China Evergrande, where following our earlier reports (see below) that a bank run emerged among creditors of the biggest and most indebted Chinese developer as its bonds were no longer eligible collateral in the repo market after a ratings downgrade, on Monday the rout went from bad to catastrophic as various Evergrande bonds crashed amid a liquidation frenzy, prompting China’s stock exchanges to halt trade.

This article was originally published by ZeroHedge.

The Shanghai Stock Exchange said in a statement that it had temporarily suspended trading in China Evergrande Group’s 6.98% July 2022 corporate bond following “abnormal fluctuations.” The exchange had also suspended trading in the bond on Friday.

Shanghai exchange data showed the bonds sliding more than 25% to a low of 40.18 yuan after the resumption of trade on Monday afternoon. The company’s 5.9% May 2023 Shenzhen-traded bond , which was also suspended, fell more than 35% after trading resumed. China Chengxin International Credit Rating Co (CCXI) downgraded Evergrande and its onshore bonds to AA from AAA on Thursday, and placed the company and its bonds on a watchlist for further downgrades, effectively freezing the company out of the repo market.

The endgame for Evergrande started on Friday, when China Securities Depository and Clearing Co. (CSDC) reduced the “conversion ratio” of the July 2022 bond to zero, effective Sept. 7. Other Evergrande bonds were not included in CSDC’s table of conversion ratios on Friday as they no longer qualified for inclusion. The conversion ratio determines leverage limits for repo financing given a specific bond pledged as collateral. CSDC is owned by the Shanghai and Shenzhen stock exchanges. In other words, Evergrande suddenly finds itself with zero access to the repo market which funded it to the tune of billions heading into Friday.

According to Reuters, a director at a local brokerage said that the reduction in the conversion ratio was a “grey rhino” – a highly obvious yet ignored threat. “It was bound to happen.”

Evergrande declined to comment. But in a statement on the Shanghai Stock Exchange on Monday, it acknowledged the impact of the rating downgrade on the bonds’ use as pledged repo collateral. It said the bonds had previously been deemed appropriate only for qualified institutional investors, and the downgrade had no impact on investor suitability.

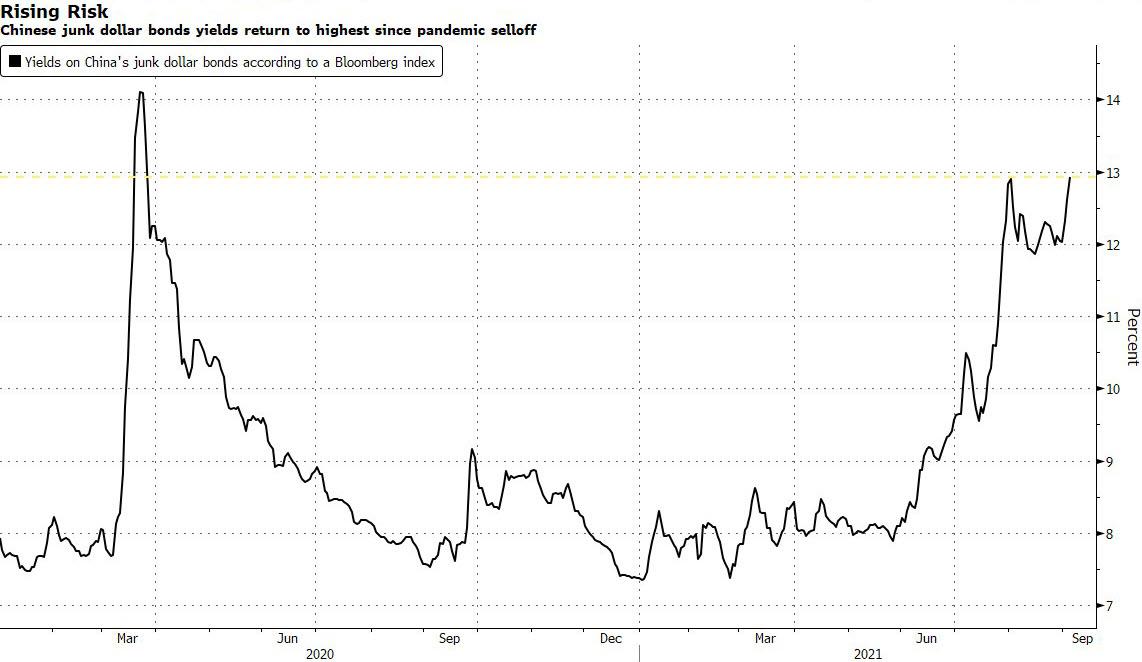

Worries surrounding Evergrande, which has been scrambling to raise funds to pay lenders and suppliers, have grown into broader concerns that a debt crisis could send shockwaves through China’s banking system. Indeed, on Friday, an index of high-yield Chinese dollar issuers fell to its lowest level since spring 2020.

Overnight contagion spread to other Chinese dollar junk bonds, which were hammered amid concern that the liquidity crisis at China Evergrande Group will worsen, raising the cost of borrowing for real estate companies. Yields on the notes, which are dominated by property firms, rose to 12.9% on Friday, Bloomberg reported.

That was the highest since March last year when concern over the coronavirus pandemic roiled markets. The broader selloff continued Monday with the bonds falling as much as 0.5 cent on the dollar, according to credit traders.

With tougher rules on leverage and a regulatory crackdown on the property market weighing on indebted real estate companies, Moody’s last week cut its outlook on the industry to negative from stable, and said falling sales, liquidity and cash flows will increase refinancing risks for weaker developers in particular.

Property firms need to repay or refinance some $14.6 billion in dollar notes maturing through the end of this year. Dollar bond sales in August by Chinese developers were the lowest since the lunar new year lull in February, and were just 14% of January’s volumes, Bloomberg-compiled data show.

As noted below, Evergrande warned last week it risks defaulting on its debt if asset disposals fail to materialize. The company said on Friday contracted sales, including those to suppliers and contractors to offset payments, dropped 26% compared with a year ago.

With Evergrande’s collapse now a question of when not if, concern is building about the financial health of other Chinese developers, including Fantasia Holdings Group Co., Central China Real Estate Ltd. and Guangzhou R&F Properties. Moody’s lowered its rating on Guangzhou R&F by one notch to B2 on Friday and put the builder on watch for further downgrade, citing increased refinancing risks. Guangzhou R&F’s note due 2023 is at 58.4 cents after plunging 18.7 cents last week.

The firm has a $200 million dollar note maturing Sept. 27, while Fantasia has $752 million in offshore bonds coming due through the end of the year including $208 million due in October, Bloomberg-compiled data show.

* * *

Just days after Evergrande’s bonds hit new all time lows after “China’s Lehman” warned that the company with over $300 billion in debt and which many view as systematically important for China, the selloff accelerated further following news of a mini bank run as i) several key creditors demand immediate repayment and ii) as Evergrande bonds are no longer accepted as collateral.

As Bloomberg first reported last Friday, at least two of Evergrande’s largest non-bank creditors have demanded immediate repayment of some loans, adding a liquidity run to the growing insolvency strains at the world’s most indebted developer. The two creditors are trust companies which pool money from wealthy individual investors and have been a major source of “shadow” financing for Evergrande and other Chinese developers.

The trusts sent repayment notices to Evergrande over the past two months after becoming concerned about the property giant’s financial health. Trust loans often include terms that allow creditors to demand early repayment if certain conditions are met, such as sales targets, ratings downgrades or lawsuits. One of the trusts has so far received only a small portion of the money owed by Evergrande, Bloomberg reported. The size of the loans involved couldn’t immediately be learned.

The start of a bank run at Evergrande is the latest sign that China’s most indebted property developer will inevitably default on $305 billion of liabilities to banks, shadow lenders, suppliers and homebuyers unless Beijing bails it out similar to the last-minute rescue of China’s bad debt giant Huaron, which recently got a thumbs up from Beijing. However, in the case of Evergrande, so far authorities have yet to blink – despite the potentially cataclysmic consequences of a default – and as a result the developer’s bonds have plummeted to levels that suggest investors are bracing for a default.While Chinese regulators have urged the company to resolve its debt woes, the government has so far stayed silent on whether it will provide financial support.

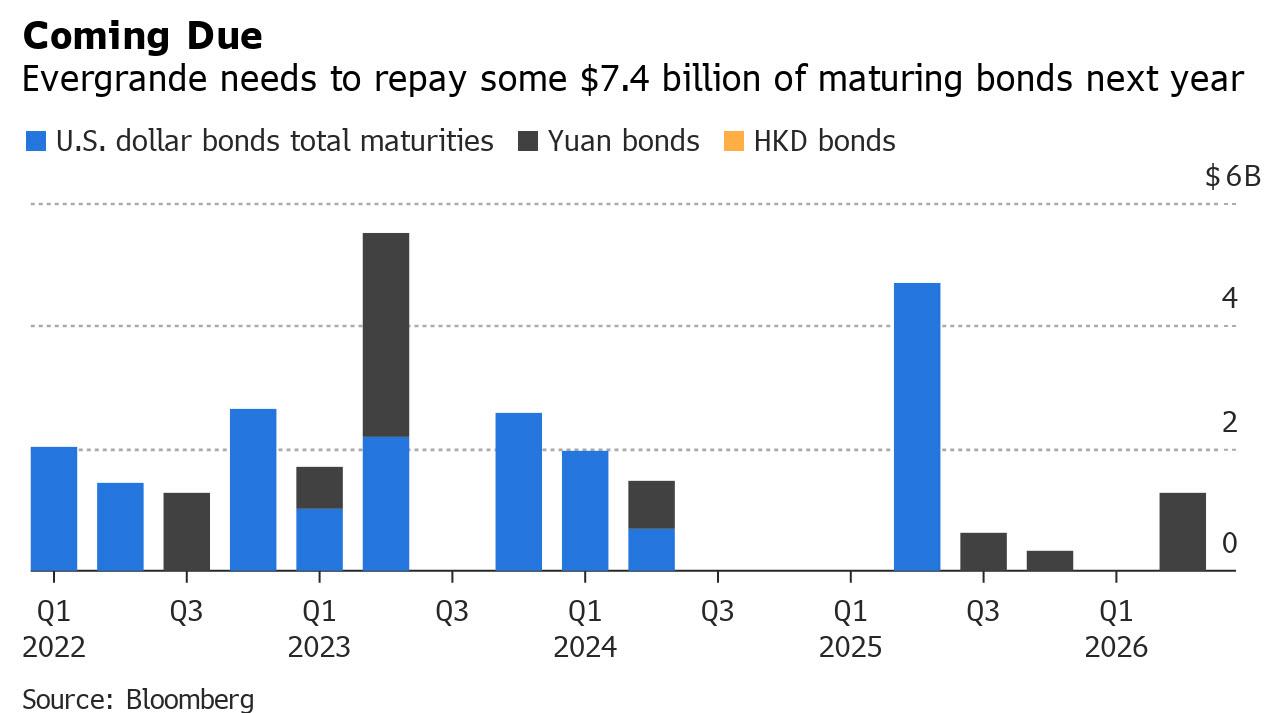

As Bloomberg adds, “shadow” trusts have been a significant source of funding for Evergrande, accounting for about 40% of borrowings at the end of 2019, the last year the company disclosed the figures. While trust lending to developers has slowed in the past year, Evergrande has about 46 billion yuan ($7.1 billion) of such loans maturing in 2021, according to data complied by Yongyi Trust Research. About 11 billion yuan is due in the fourth quarter, and another $7.4 billion is due in 2022. And should the company survive to 2023, that’s when it gets really tough.

A failure to repay – which now appears inevitable – could prompt at least one trust to call back all its loans, though it’s unclear how Evergrande would respond. Court cases against the company and its affiliates are being centralized in Guangzhou, a city in Evergrande’s home province of Guangdong, making it more difficult for creditors to freeze assets or pursue repayment through other local courts.

However, the bank run hammering the company’s dollar bonds is just the start.

Also on Friday, Bloomberg reported that Evergrande’s yuan bonds are no longer accepted as collateral in the country’s key funding market, cutting it off from another critical source of funding – the repo market – and adding to signs of increasing default risk.

Evergrande’s notes were absent from a list of securities accepted in return for cash in so-called repurchase agreements on Shenzhen’s exchange. They also couldn’t be pledged for cash on Shanghai’s exchange, according to a notice posted by the clearing house late Friday.

The clearing house’s daily notice, which covers on-exchange transactions only, previously featured six of Evergrande’s onshore bonds for use in Shenzhen’s repo market, and three for transactions in Shanghai. Most pledged repo deals still occur in China’s interbank market, where there’s little transparency.

The move came after China’s largest credit-rating assessor cut the developer’s onshore unit to AA (the functional equivalent of a A for China’s massively grade-inflated credit rating system) from AAA – as well as nine of its yuan bonds – and put them on a watch list for potential further downgrades. That makes Evergrande bonds issued after April 2017 ineligible as collateral, according to clearing house rules, though the China Securities Depository and Clearing Corp. has the final say.

The latest set of catastrophic news for the Chinese property developer – which has been struggling to convince investors, suppliers and creditors it can generate cash to make good on liabilities after payables rose to a record – was the straw that finally broke the camel’s back and on Friday, trading in several of Evergrande’s thinly-traded onshore notes was briefly halted on Friday to steep declines, while some of its dollar debt trades below 30 cents. The shares have lost 74% this year to the lowest since July 2015.

Needless to say, the countdown to insolvency has begun even as Evergrande has been rushing to liquidate assets and raise funds – with the company’s core property business losing record amounts of money, construction on some projects halted by suppliers and freely available cash at a six-year low, the company warned of a potential default if asset-disposals fail to materialize, and reiterated plans to sell stakes in its listed electric-vehicle and property services units.

None of that will help, and at this point the collapse of Evergrande is just a matter of time and the only questions are i) whether Beijing will step in, and ii) how bad the avalanche of adverse consequences will get.