Most NFL general managers (GMs) are optimistic and displaying overconfidence today as they prepare for tomorrow’s NFL draft. The draft is a once-a-year opportunity for GMs to acquire talent.

This article was written by Michael Lebowitz and originally published by Real Investment Advice.

Like investors, GMs often think they are smarter than their competitors, aka the market. Yet, they frequently have similar mindsets and follow the same narratives that drive their competition.

As we will share, overconfidence and groupthink among football GMs and investors are behavioral flaws that often harm performance. Having the tools and strategies to mitigate our behavioral traits is extremely valuable and can lead you to better returns.

Overconfidence In The NFL

Four of the first five picks in the draft are expected to be quarterbacks. Not only is the quarterback the most important position on the field but this year’s draft is hyped as having several future greats.

Based on data from Warren Sharp, an NFL analyst, most of the quarterbacks taken in the early rounds will be average. His Fox Sports article entitled The success rate of first round QBs makes Lamar Jackson’s case for him, quantifies just how poor the odds are of drafting the next Super Bowl-winning quarterback.

There have been 38 quarterbacks drafted in the first round since 2011, the year the NFL changed the collective bargaining agreement.

These 38 first-round quarterbacks have made a total of 1,909 starts. Their record? 1034-1035-7.

He claims that of those 38 quarterbacks, only one, Patrick Mahomes, has won a Super Bowl. Furthermore, of the 28 from that group who are no longer on their initial contracts, the average time they were a starter was a mere 3.4 years.

Despite the proven mediocrity of quarterbacks taken in the first round, we have little doubt that overconfidence will be on full display by the GMs drafting quarterbacks with their top picks after they make their selections.

Groupthink In The NFL

This behavioral trait arises when people seeking conformity think and act similarly. Typically, groups reach a consensus opinion without proper evaluation and with minimal alternative viewpoints.

For instance, it is widely accepted that the four quarterbacks likely to go in the top five, Williams, Daniels, Maye, and McCarthy, will be excellent pros. Most NFL analysts offer differences between the quarterbacks but praise the physical and mental traits they believe will make them NFL starts. Very few analysts have poor ratings on any of those four quarterbacks.

Choosing one of the four quarterbacks is comforting. Simply, GMs have cover if their pick is a dud. Who could have known? Every expert thought he would be a superstar!

Investor Overconfidence And Groupthink

Replace players with investment ideas and GMs with investors. The overconfidence and groupthink mentality impacting GM draft day decisions are similar to those investors always face.

We quantified the odds of GMs picking above-average quarterbacks earlier. Per DFA Funds, the odds of an investor outperforming the market are even more daunting.

We saw from the data above that an investor has about a 75% chance of underperforming the market in any given year, which means you have a 25% chance of beating the market in any given year.

The message to take away from that statistic is to leave your confidence at the door!

Regarding groupthink, most investors, like GMs, find comfort in knowing that many other investors are doing the same thing. Market narratives are a form of groupthink. Narratives help explain market movements and trends. Often, a narrative develops after a trend has started. In other words, rightly or wrongly, the narrative is the rationale.

Today, narratives appear to be quicker to form and longer lasting. Maybe the advent of social media has allowed for their quicker dissemination and growth.

Narratives describe the mindset of a group of investors. When you unknowingly invest based on a narrative, you are likely setting yourself up for failure.

Strategies To Combat Behavioral Traits

Appreciating that GMs have a one in three chance of successfully using a precious top-five draft pick on a quarterback or that only a quarter of investors will beat the market, we best have tools to manage our behavioral traits and improve our odds of success.

Zig

Warren Sharp advises GMs to “zig while others zag.”

To zig is to have a contrarian mindset. For instance, it’s important for your portfolio to have popular stocks leading the market higher. But at the same time, understand that confidence can wane quickly, and a new set of stocks will take the throne soon enough. Don’t overstay your welcome in a narrative.

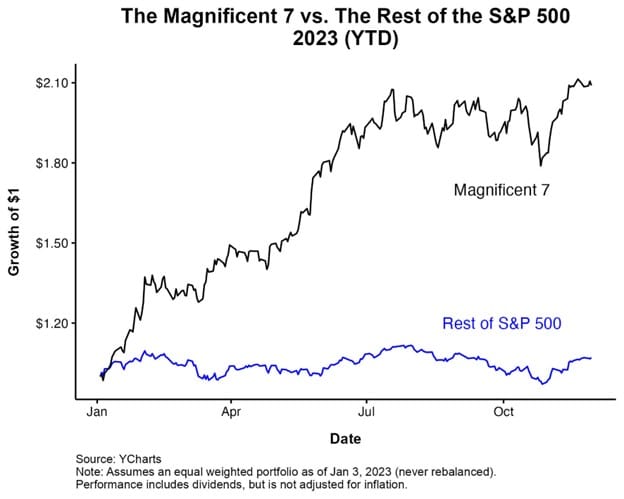

It wasn’t that long ago that the Magnificent Seven stocks were all the rage. Their returns handily beat almost every stock and index. Holding a meaningful subset of the seven stocks was vital to keep up with the broad market indexes. However, the Magnificent Seven’s period of outperformance has either ended or is on pause. But, the narrative still thrives, and whether it’s already happening or will occur shortly, investing in the aged groupthink will catch many investors offside.

Take Profits

It’s hard to sell when others are buying. Still, when the narrative-driven stocks fall out of favor, the prior profits and reduced position sizes will bolster returns and lessen the risk of underperforming the market.

Appreciating what the market, and not popular narratives, tell you is equally vital. For instance, have you noticed that utilities and energy are the best-performing sectors lately? Those solely holding the Magnificent Seven and neglecting other sectors are falling behind.

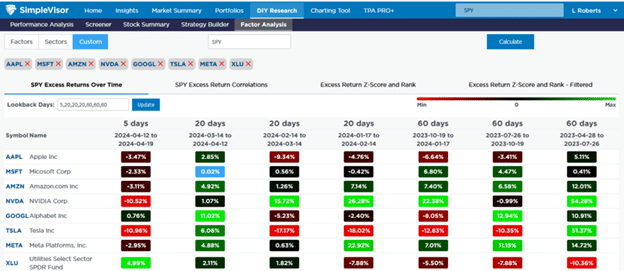

The SimpleVisor table below shows the relative performance of the Magnificent Seven stocks and XLU, the utility ETF, versus the S&P 500 over various time frames. Other than NVDA, most of the seven have been underperforming the market as of late. Also, the once poorly performing utility sector has been beating the market for the last 45 days. Selling the Magnificent Seven 45 days ago to buy utilities would go against groupthink, but it was a smart call.

Appreciate Your Options

The GMs with the top five picks have a precious option. Instead of picking a quarterback with limited odds of success, they can trade the pick to another team. In exchange, they might receive multiple high-level draft picks, boosting the odds of success.

Other positions in the NFL draft have much better success rates than quarterbacks. If a GM can set aside their confidence in their ability to pick the right quarterback, they can increase the odds that they could easily land at least two very good players and possibly a pro bowler. Maybe they can even use one of the picks to get a quarterback in the later rounds. Let’s not forget Brock Purdy, the San Francisco quarterback who led the 49ers to the Superbowl, was Mr. Irrelevant, the last person taken in the draft.

Investors have options, too. Many stocks, sectors, and factors will likely outperform the market but do not fit the narrative du jour. While buying what others aren’t may be uncomfortable, it may be more profitable.

The other lesson is to diversify. Putting most of your eggs in one basket can significantly impact your relative performance. You will underperform if you are proven wrong, as is most common.

Let Winners Run

One of the most popular Wall Street sayings is, “Cut your losses short and let your winners run.”

If our chances of beating the market are one in four, doesn’t it make sense to trade your portfolio actively? Many investors do the opposite. Their confidence and the attraction of groupthink keep them in underperforming stocks. At the same time, alternative stocks that are less followed may be the best bets.

It can be appropriate and profitable at times to follow the crowd. However, at all costs, don’t ignore alternative views.

Summary

We risk underperforming the market by falling victim to our natural behavioral traits. Therefore, we owe it to ourselves to entertain and understand alternative views. As odd as it may seem these days, we need to watch FOX News and read the New York Times. We must challenge ourselves to understand better things that may not be comfortable.

Seek out and study the views of others with whom you disagree. By better understanding opposing opinions, you will strengthen your existing views or better recognize flaws in your current logic. Either way, an investment thesis is better for it.

Most importantly, remember that you are only human. The Patrick Mahomes of the investment world are few and far between. At times, overconfidence is a good trait, but it can also be a critical flaw.