Image Courtesy Of Schiff Gold

As interest rates rise, the air continues to hiss out of the housing bubble.

Existing home sales tumbled to a two-year low in May. Sales fell to a seasonally adjusted 5.41 million units, according to the latest data from the National Association of Realtors. It was a 3.4% drop, bringing existing home sales to the lowest level since June 2020. May was the tenth consecutive month of year-over-year declines.

This article was originally published by Schiff Gold.

Year on year, sales of existing homes have tumbled by 8.6%.

According to the National Association of Realtors, “Further sales declines should be expected in the upcoming months given housing affordability challenges from the sharp rise in mortgage rates this year.”

With sales falling, housing inventory is starting to creep higher. The supply of existing homes jumped 12.6% in May.

According to the NAR, it would take 2.6 months to exhaust the current housing inventory. That’s up from 2.5 months a year ago. But inventory remains relatively tight. Analysts view a six-to-seven-month supply as a healthy balance between supply and demand.

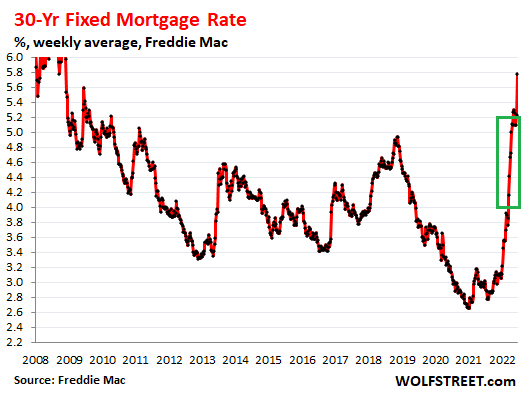

Rapidly rising mortgage rates have put the squeeze on prospective homebuyers. The average 30-year fixed mortgage rate has spiked to 6.1%. It’s the first time we’ve seen mortgage rates over 6% since the crash of 2008. Until mid-April mortgage rates were in the 4% to 5% range. Just one month ago, rates were 5.49%.

We won’t begin to see the impact of the latest leg up in mortgage rates until we get the June housing numbers. As WolfStreet explains, “The closed sales in May are based on deals that were largely negotiated in April, with mortgage rates from April and before, when these buyers applied for mortgages and obtained mortgage rate locks that are good for a set period of time. The green box shows the mortgage rates that roughly applied to home purchases that closed in May, around 4% to 5%.”

While sales have dropped and inventory is rising, housing prices still haven’t dropped significantly. The median existing-home sales price exceeded $400,000 for the first time in May. That represents a 14.8% increase from a year ago.

This number is skewed upward because lower-income homebuyers have been priced out of the market by spiking mortgage rates. The houses that are selling tend to be in higher price ranges. As the California Association of Realtors noted, price increases “can largely be attributed to the mix of sales, with the high-end market continuing to outperform the more affordable market segments.”

Prices will likely drop as sales continue to plunge, but a crash in housing prices is unlikely given that inventory remains relatively tight. A more likely scenario is a stagnating housing market with few sales and few houses on the market.

While we may not see the kind of crash we saw in 2008, a housing market bust will reverberate through the economy as rising housing prices squeeze Americans already struggling to make ends meet.

With the Federal Reserve pushing its base rate up 75 basis points, you can expect mortgage rates to continue their rapid upward climb. As Reuters noted, the housing market is “the sector most sensitive to interest rates,” and it is losing speed. But they spun this as good news.

“Its slowdown could help to bring housing supply and demand back into alignment and slow price growth.”

This leaves one question unanswered: why is supply and demand “out of alignment” to begin with?

In a nutshell, it is just one of the many economic distortions caused by the government and the Federal Reserve’s response to the pandemic.

The Fed blew up this housing bubble when it artificially suppressed interest rates and bought billions of dollars in mortgage-backed securities. Now the central bank has pricked the bubble by pushing rates up.

What the Fed giveth, the Fed taketh away.

Mortgage rates began to fall in late 2018 as the economy tanked and the Federal Reserve ended its post-2008 rate hike cycle. Rates continued to fall as the Fed pivoted back to quantitative easing and then dropped through the floor with the rate cuts and QE infinity in response to the coronavirus. The big spike in mortgage rates we’re seeing today started as the Fed began talking up monetary tightening to tackle raging inflation.

We expect the housing bubble to continue to deflate as we move through 2022. Just how fast the air comes out and the impact on the broader economy remains to be seen.

Ownership of AI and control of personal data are no longer abstract questions for techies… Read More

Faith institutions already own land and want to help address community needs — can this… Read More

The U.S. economy grew 2.1% in real terms in 2025, but that national figure tells… Read More

Much of the concern surrounding artificial intelligence is about power: the technology’s economic power to… Read More

Cuba fully restored its energy grid early Wednesday after the third nationwide blackout this year, but… Read More

Up until now, the politicization of AI models generally ran in one direction with US… Read More

This website uses cookies.

{kind=link}