Image Courtesy Of Real Investment Advice

In 2023, the “Magnificent Seven” (NVDA, META, TSLA, AAPL, MSFT, AMZN, and GOOG) became a popular nickname for the seven largest stocks by market capitalization. “Magnificent” was used because these stocks led the S&P 500 higher throughout the year. These same stocks had a strong showing again in 2024, as all seven were among the top ten contributors to the index that year. It’s fair to say that investing in the Magnificent Seven was one of the best strategies and most popular trends during those two years.

This article was written by Michael Lebowitz and originally published Real Investment Advice.

Thus far in 2025, the value of the Magnificent Seven strategy is fading. Only three of the Magnificent Seven stocks are among the top ten contributors to the S&P 500. That compares to all seven in 2023 and 2024.

Perhaps the fad is taking a brief hiatus, and the seven stocks will soon regain their lead. Or maybe the trend is shifting.

Given the importance of the seven stocks to the broader market, it’s worth examining them.

2025

The graph below shows that only three of the Magnificent Seven stocks are beating the S&P 500 through early July. Furthermore, Apple and Tesla are lagging the S&P 500 by 20% or more. Google is underperforming the index by 14%, while Amazon shares remain flat for the year in an up market. The other three stocks, META, MSFT, and NVDA, are outperforming the index handily, but not as significantly as they did in 2024 and 2023.

The AI story has been a dominant theme this year, but that theme has not benefited all companies related to AI. For instance, Google and Amazon are major players in the AI space, yet both stocks have lagged the market. At the same time, Meta, Microsoft, and Nvidia are outperforming the market, partly due to their significant exposure to AI. Apple shares, as we wrote in Crisis at Apple, are falling woefully behind as they lag in the AI race. Tesla will undoubtedly benefit from AI, but Elon Musk’s political ambitions and weak car sales are weighing on its stock price.

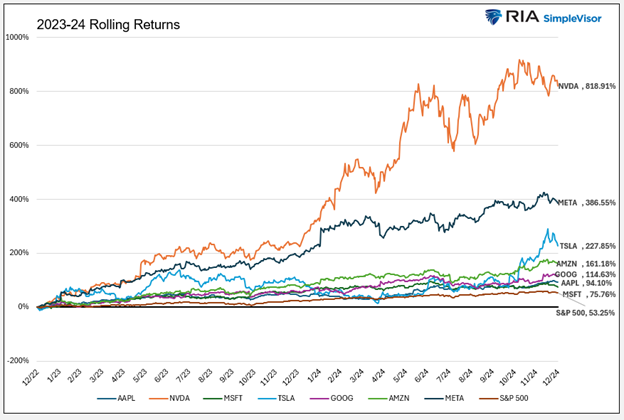

2024 and 2023

The graph and table below illustrate the remarkable outperformance of all the Magnificent Seven stocks in 2023 and 2024. The “worst” of the seven, Microsoft, still outperformed the S&P 500 by 22% over the two years. Others like NVDA, META, TESA, and AMZN lapped the market many times over.

Consider the following:

Market Volatility in 2025

To appreciate why 2025 is a far cry from the two prior years for the Magnificent Seven, it’s essential to consider that volatility is significantly elevated compared to 2023 and 2024. In 2025, only halfway through the year, there have already been six days in which the market increased or decreased by more than 2% in a single day. In 2024, the number was three, and in 2023, it was zero.

The graph below charts the S&P 500 ETF SPY against realized and implied volatility. As it shows, implied volatility was very low from mid-2023 through mid-2024. After that, implied volatility became more volatile. Unlike implied volatility, realized volatility was subdued until it spiked on April 5th, Liberation Day, and stayed elevated until recently. Both implied and realized volatility have reverted to early 2025 levels.

Magnificent Seven Correlation

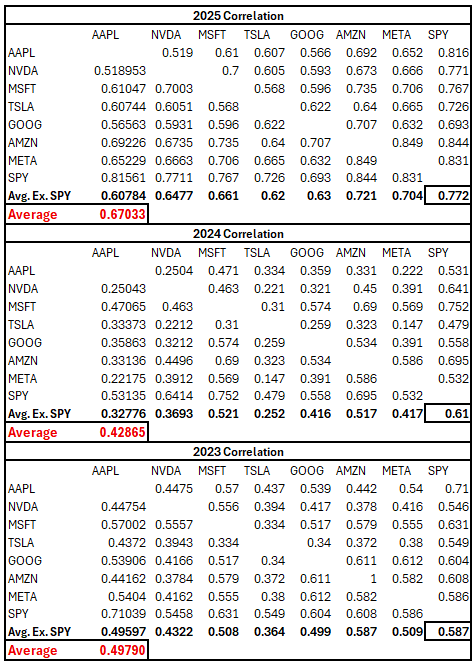

Interestingly, despite the significant divergences in performance between the Magnificent Seven stocks and the increased volatility in 2025, the share prices are more correlated than in 2023 and 2024.

That doesn’t sound logical, but consider that correlation measures how well prices move in the same direction with each other or not. Often, in high-volatility regimes, stocks of all types tend to move in the same direction. For instance, on large up days, it’s not uncommon for 90% or more of the S&P 500 stocks to be in the green. Similar for significant declines.

Thus, with increased volatility comes more days in which all the Magnificent Seven stocks are up or down. That, however, does not mean the magnitude of the changes is the same. Simply, we shouldn’t assume that higher correlations between the stocks mean similar performance.

The tables below show the correlation between each Magnificent Seven stock and the S&P 500 (SPY). As shown, the average correlation among the stocks is running at .67 this year, compared to sub-50 levels over the last two years. Similarly, their average correlation to the S&P 500 is high at 0.77, up decently from the 2024 and 2023 levels.

The Magnificent Three and Speculative Stocks

The Magnificent Seven are not in vogue as they were in 2023 and 2024. While NVDA, MSFT, and META are performing well, it appears that a new crop of more speculative, higher-beta stocks is leading the market.

Might this represent a new phase in the bullish rally from the 2020 lows? In other words, is the market shifting from high-growth, large-cap companies with substantial revenues and earnings to smaller, more volatile companies with less fundamental support but prospects for exponential growth?

A similar shift occurred in the late 1990s. As the dot-com bubble expanded, market leaders shifted from larger, more established companies to smaller ones with hopes for massive growth.

The recent trend has not been happening long enough to claim that this is the case, but the change in leadership warrants attention.

Summary

Market trends are constantly shifting. To that end, the recent relatively weak performance of the Magnificent Seven, in aggregate, may point to a new trend. Time will tell if the laggards in the Magnificent Seven are taking a well-needed break or if an actual change in leadership is coming.

If this is the melt-up phase of the bull market and speculative, high-beta stocks take the leadership role, we might expect volatility to remain high. Furthermore, while a melt-up usually ends poorly, the bull market ending is not necessarily imminent. As Bob Farrell stated:

Exponential rapidly rising or falling markets usually go further than you think, but they do not correct by going sideways.

We are not yet ready to call this the melt-up phase of the post-pandemic rally. However, we are paying close attention to the market tone and changes in trend to understand better the type of environment we may be dealing with this year and into early next year.

U.S. phone customers pay more than $340,000 a year for an Anchorage company to keep… Read More

If you've lived in Ventura County for several years, you've probably noticed that the community… Read More

The 2026 FIFA World Cup is awarding $655 million in performance prize money, making it the richest… Read More

SpudCell is a big step toward synthetic biology's dream of building life from scratch. Synthetic… Read More

If you knew you were standing inside a stock market bubble, you wouldn’t be standing… Read More

A nationwide credit card outage in Japan disrupted shop payments, rail pass purchases and Mobile… Read More

This website uses cookies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}